XBRL Definition

eXtensible Business Reporting Language (XBRL) is an open internet standard built on an XML base. While XML and HTML are functionally similar, for data transfer, analysis, and preservation, XML offers more convenience and flexibility. XBRL’s main goal is to lower the overhead of data exchange, and simultaneously raise the accessibility of information. Through the internet,XBRL provides more timely access to information and increase its ultimate utility. XBRL creates standardized environment where users can use the internet to prepare, broadcast, exchange and analyze financial information. n addition to XBRL’s automated financial data exchange and extraction being independent of information systems and software limitations, XBRL also reduces the need for different formats and input duplication. This allows users to compare and retrieve financial information directly,resolving the problem of inability to directly compare financial information in different formats.XBRL helps reduce costs related to financial reporting preparation, and creates more opportunities for investors and analysts to access financial information, and enhances the integrity and comparability of of the business reporting information.

XBRL Business Case

The purpose of establishing XBRL is to allow corporate financial information to be transmitted more quickly and accepted more readily, across different uses of said information. At the same time, the preparation, use and financial intermediary for the information can be grouped into separate groups for the greater efficiency.

First、General business use.

XBRL technology can be applied not only in the preparation of financial statements, but also in publishing or uploading information related to the competent units on the financial environment. This is a completed platform which dispels the need for users to make further efforts, and there is no need to disaggregate the implementations of a number of information processing operations. XBRL exists to expedite the preparation of financial statements to increase the enterprise efficiency. At the same time, in light of restrictions in the enterprise information system from the platform that may be required, including costs incurred in buying both hardware and software, XBRL does not increase the demand for additional upgrades to their business systems; it allows corporations the liberty to choose whichever platform they prefer.

Second、The investing public

For the investing public, the business use of XBRL allows investors to more quickly access business-related materials, and at the same time, directly access information for comparative analysis to avoid re-entering the data inefficiently. In addition, corporations can also leverage XBRL to make it easier for investors to access the company's financial information, to increase the quality of their investors’ decision-making.

Third、Investment analyst

To the analyst, in addition to quicker and more accurate disseminated financial information, the use of XBRL will contribute to the analysis of the company's financial information because the information has become more detailed, more searchable and provides more convenient access to the Internet which can be used to analyze the data. XBRL users can also choose the output format that is needed, which in turn improves the efficiency of the whole exchange of information. Analysts can save data processing time, and use their resources in the professional study of decision-making information and provide more value-added services.

Forth、Securities unit management

Since 1999 the Ministry of Finance of the Securities and Futures Commission has actively promoted the "declaration of open file electronic information network." In addition to providing information to the Securities Fund, this requires financial bodies (public companies, securities dealers, futures, securities investment trusts, securities investment advisers and financial securities, etc.) to be annually consistent with their information and provide digital copies of their public information to the Securities fund. The purpose is to force the stock market to provide more complete information available to investors. However, during the implementation process companies often upload files in different formats (such as Adobe Acrobat's PDF file or DynaDoc of WDL file format, and so on) even within the same company, which obviously results in user inconvenience. If companies are to adopt a unified XBRL format, the information and data can be uploaded following a series of standard steps, and the companies would upload files with the same format. Upon direct inspection, comparative analysis, the management of the securities unit, within a permitted period of time, will be able to achieve public information transparency and fairness of the securities market with minimal cost.

Fifth、Government agencies and non-profit organizations

For the management of a large number of enterprises and related documents and forms of public service agencies, the government can utilize the XBRL standard format and forms to enhance their effectiveness. The government can create public websites with information forms for users to fill out to ensure they can collect information in a standard format with greater efficiency. In addition, government agencies and non-profit organizations have numerous finance related documents and forms, each one requiring their own formats, however, if they were to adopt a unified XBRL standard for their reporting, each of these forms would be more streamlined, thus achieving administrative reform and enhancing their effectiveness and performance.

Sixth、Accounting Industry

For the company's accountant , as XBRL can be applied to a variety of information on the company's transmission, in regard to the financial statements of accountants should play a role in counseling clients to provide relevant training to enhance the competitiveness of the customer, not only to open up another accountant’s bBusiness opportunities and will also enhance the professional accountants. In addition, the business gradually in the future on the Internet to publish their financial information, the firm will face the need to check the Internet for information on demand, and the use of XBRL to expose the benefits of unification, that is, we do not need to manually format different interpretation The information directly through the standard application made by customers of financial disclosure, and in the future if further business with the reunification of the trajectory of the audit database link, in determining the system to control all aspects of a good and correct logic, then dDirectly through the Internet to check for continuity of work, so a large number of manual operations can be reduced to increase the efficiency of the check, check and improve quality .

Seventh、Financial information systems integration industry

Integrated financial information system operators most fear their technology, forms and databases will not be able to communicate with multiple platforms and each other. XBRL was formed with this issue in mind, creating a low cost and high quality solution for financial information systems to integrate two separate systems. Data can be input and output with the XBRL-based unified format and type, so it will be easily integrated across heterogeneous systems and platforms.

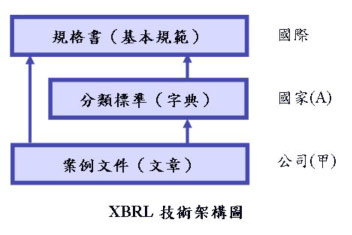

XBRL Technical Structure

XBRL國際組織(XBRL International)提出XBRL三階段技術架構:第一,規格書(specification)制訂階段,由XBRL國際組織所制訂;第二,分類標準(taxonomy)建立階段,原則上由各國之會計權威機構所制訂;第三,案例文件(instance documents)編製階段,由各財務報表個體編製。

一、規格書

XBRL規格書是所有XBRL文件之基礎,包含分類標準以及XBRL案例文件在內,都應依照規格書之內容加以制訂或編製。規格書的內容,主要在定義一份XBRL分類標準與文件的格式、各種元素(elements)的定義以及資料型態(item type)。各國並無規格書的制定權,統一由XBRL國際組織負責制訂,只能於訂定其分類標準或產生案例文件時選擇規格標準版本。

二、分類標準

XBRL分類標準是由各國之會計權威機構,依據XBRL規格書與各地會計準則所制訂,以提供XBRL案例文件之編製者,根據分類標準中所定義之元素名稱與屬性,編製XBRL案例文件。

三、案例文件

當會計權威機構制訂了符合當地會計原則之分類標準後,各個欲採用XBRL揭露其財務資訊的企業,便可以利用此分類標準,配合XBRL組織所制訂之規格書,編製企業報告之XBRL案例文件。

參考資料:XBRL示範平台 周濟群老師

Function of XBRL

First、Preparation of financial statements and transfer

The main purpose of XBRL is to promote the convenience of financial reporting through information technology. Financial systems statements reporting via databases over the internet will be streamlined through exchange and analysis of information, also creating more convenient and accurate financial statements both on paper and online. This will be more effective than the current method, and also make the transmission of such information more fluid and effective .

XBRL will be used to prepare financial statements with more in-depth and detailed information, and thus investors can make prudent and timely decisions, as well as obtain precise and relevant data and not the Bi-Suite enterprises that require manual searches to retrieve their intended data.

Second、 the preparation of tax returns

Because of the direct input of corporate tax data from the company's financial statements prepared in the same database, XBRL has no need for an outside solution to organize and transmit the data through the internet to the Tax Bureau. This makes tax payment convenient by allowing taxpayers to avoid having to pay taxes in person, allowing people to avoid physically going to the tax bureau and avoid the long queues and save effort and time.

Third、 Authorities requested the preparation and delivery of financial statements

Based on domestic regulations on financial reporting, a company must issue statements on finance related issues, such as quarterly bulletins, annual reports, and inside trading; this is in addition to declaration of securities. Furthermore, the company should also issue a copy of the document to the following organizations:

- Taiwan Stock Exchange;

- Taipei Exchange;

- Taiwan Securities Association;

- Securities and Futures Market Development Foundation.

Based on the principle of public information, XBRL can allow businesses to declare required financial information in a fixed format to the relevant authorities. If the requirements of businesses use XBRL , related to the financial statements, transfer efficiency and accuracy can be improved , and at the same time the cost of finishing the work will be reduced.

Fourth、Management and financial statements and the preparation of delivery

Companies often have their own in-house internal operating statements for information analysis, and in some cases must be inter-departmental information, but even if the implementation is regarding e-business, the Information Technology department must maintain private and not share the information with other departments. The reason is that , because this use software and data does not necessarily have the same level of security or may not be able to be used together. The current method, which is expensive , uses Enterprise Resource Planning System (ERP) to achieve the desired objectives. However, the small and medium-sized enterprises are faced with such data incompatibility issues, and they may not be able to afford the expensive ERP system . The use of XBRL, or XML interface application interface programs of information technology will become an alternative to build a low-cost and cross-platform new solutions.

Fifth、Accou nting and documentation related to the preservation of law and transfer :

XBRL also has the ability to preserve the financial documents in the long term. Because accounting literature and other documents in accordance with relevant laws have to go through dedicated information processing software to be read, only the general browser can decipher these documents.These documents cannot be read with the naked eye or even understood. XBRL documents use ASCII code to archive only, and support the use of ASCII code that can be read or modified on a simple word processor. Increasing the readability of the information in the future and maintenance of that utility is very applicable to long-term preservation of these documents. In addition, if the definition of open standards and reference model can be incorporated into describing these documents, help files and efficient searches in the use of XBRL and as a result are based on XML, it can be an XBRL document that is produced for data set, and that in turn defines the nature of the content of the labels. So search results will be more precise, and its cross-platform, compatibility, and scalability advantages will be of more help to convey a wider range of documents.

XBRL Overseas Application

目前各國已有大量之XBRL應用,以下將各國應用按金融監理領域、資本市場領域、稅務申報領域、管理監督領域,分項說明:

金融監理領域

由於金融監理需要進行大量的資料勾稽動作,因此是XBRL在實務應用中發展最快速,也是成效最卓著的領域,目前國際間如美國、歐盟、日本、西班牙等國均開始採用XBRL作為金融機構申報的資料格式。以下就美國FFIEC、歐盟COREP與日本BOJ等成功應用案例進行簡單說明:

資本市場領域

XBRL在資本市場的應用在最近幾年相當受到重視,尤其以美國SEC宣佈投資5400萬美金更新現有的EDGAR資料庫,建構以XBRL為基礎之「互動式(interactive)」新資料庫;而中國大陸上海證券交易所也在2005強制進行年報全文以XBRL格式進行報送。以下針對美國SEC、上海證券交易所、東京證券交易所與南韓KOSDAQ交易所等成功應用案例進行簡單說明:

稅務申報領域

在全球各國的稅務行政方面,經濟合作暨發展組織OECD於2004年10月初推薦各會員國採用XBRL做為稅務資料交換的核心技術,認為未來各國稅務資料申報與查核應以XBRL為優先考量之技術。此外,英國稅務局(UK Inland Revenue)業已採用XBRL作為其電子化稅務計劃的一部份。而日本稅務部(Japan NTA)則是從2004年2月起正式開始採用XBRL進行企業的税務申報(e-Tax),首先在日本國税廳所屬的名古屋國税分局内採用。而荷蘭、澳洲、愛爾蘭、德國、加拿大稅務局等均計劃採用XBRL作為公司所得稅申報格式之一。

管理監督領域

XBRL在其它政府機關的應用也很普遍,主要應用於電子化政府與工商管理方面,包括丹麥工商登記局(Danish Commerce and Companies Agency)、瑞典專利與工商登記局(Patent and Registration Office)均採用XBRL作為工商登記與公司年度財務資料的申報格式之一。愛爾蘭的主計局(Central Statistics Office)亦於2005年首度成功應用XBRL技術於其一項工商普查的計畫。英國的商業司(UK Companies House)亦於2005年開始接受中小企業以XBRL格式來申報其工商資料。而西班牙中央銀行(Bank of Spain)除了利用XBRL於其金融機構的監理以外,於2005年並同時完成了一項財務資料交換與分享平台計畫,希望利用XBRL作為其政府各部門資料分享的工具。我國經濟部商業司,於2003年亦採用XML資料格式,針對企業登記流程進行簡併與電子化。

參考資料:XBRL示範平台 周濟群老師

XBRL Adoption

推動資本市場採用XBRL計畫

一、背景說明

在資本市場全球化的趨勢下,投資人對財務資訊的要求日益提高,由於各國間並非適用一致的會計準則,加上企業網路揭露呈現的格式或方式不同,增加了資料再利用及分析比較的困難,因此國際投資人迫切希望全球財務報告可以共通。

然而要達到全球財報共通的目標,需要由二方面著手,其一是全球適用一致的會計準則,目前各國已逐漸朝與國際會計準則(IFRS)接軌,我國也積極因應,刻由金管會邀集相關單位研議推動直接採用國際會計準則之計畫;其二是建立一套通用的財報資訊標準,亦即企業資訊需有統一的電子化溝通語言,而XBRL的誕生就是為了解決這個問題。

鑑於國際間提倡推動XBRL已蔚為趨勢,我國在各界人士共同努力耕耘下,XBRL的發展也逐漸展現成果,為建構一個與國際接軌的資訊公開制度,推動我國企業採用XBRL申報財務報告為刻不容緩之工作。

二、推動方式

為加速動我國資本市場採用XBRL申報財務報告,在行政院金融監督管理委員會督導下,由證交所、櫃買中心、會計研究發展基金會、各工商團體代表、會計師代表及學者專家組成「推動上市櫃(興櫃)公司採用XBRL申報財務報告專案小組」,研議本項工作之相關事宜。

三、推動方案及工作重點

「推動上市櫃(興櫃)公司採用XBRL申報財務報告專案小組」下設立六個工作小組,研議本案推動可能面臨問題之解決方案,本計畫工作重點及時程如下:

(一) 制訂分類標準:依據會計準則、相關財務報告編製準則及其他相關法規,制定適合於我國上市櫃(興櫃)公司使用之各業別財務報告分類標準,並召集公聽會,徵詢各界對分類標準之意見,據以修訂分類標準並公告由前開公司適用,暨負責後續分類標準之維護。

(二) 開發申報工具及系統:為降低上市櫃公司之成本,擬配合本案全盤規劃時程,於各階段分類標準制訂完成後,設計申報工具,免費提供上市櫃(興櫃)公司使用。

(三) 揭示系統整合:研議自願及全面採用XBRL申報財務報告時,資訊揭示系統整合等相關解決方案。

(四) 法規制訂:配合自願申報及全面申報,調整相關法規。

(五) 教育訓練及宣導活動:為利各界了解XBRL,並使公司熟悉申報工具,將加強宣導,辦理各項宣導會、研討會及教育訓練課程等項活動。

四、計畫時程

一、 短期—建置示範平台(97年底完成):證券交易所從公開資訊觀測站的資料庫中選取部分上市櫃公司的財報內容,從而轉換為XBRL格式。除此之外、證券交易所也提供互動式的交叉分析工具,讓XBRL平台可以計算常見的財務比率、跨公司同類財務資料的比較、多公司跨年度的財務資料比較等等。示範平台主要目的為針對使用者及投資人進行各項推廣活動,使其了解什麼是XBRL及如何應用XBRL的資訊,同時在此階段,也希望上市公司提前獲得XBRL相關資訊,公司內部開始進行評估及採用的準備。具體措施條列如下:

乙、 舉辦XBRL研討會及宣導會。

二、中期—鼓勵自願申報:證交所預計於2009年10月進行巡迴宣導,將徵求有意願採用XBRL的公司參與自願性申報計劃。2008年五月,交易所去荷蘭參加第17屆的國際XBRL會議,期間也與美國證管會(SEC)負責資訊申報的官員接洽,其表示美國未來將強制採用XBRL,相信將有助於台灣推廣XBRL,因為有許多台灣公司在美國上市,美國若強制採用XBRL,這些公司要在台灣自願採用XBRL應不成問題;在此階段,交易所也會提供上市公司相關資訊及訓練,並以交易所提供之具備四大表轉換功能軟體,協助上市公司完成自願申報。具體措施條列如下:

乙、 調查上市(櫃)公司採用XBRL意願及影響其導入意願因素。

丁、 設置專案服務小組提供相關輔導與諮詢。

三、長期—全面推廣採用:相信經過幾年的推廣,上市公司對XBRL逐漸熟悉,也了解如何應用XBRL,對於全面採用必然有很大的助益。目前申報採取雙軌制、以 XBRL格式與現行財報格式同時並行申報,並視實際申報情形決定何時全面限用XBRL格式申報。目前預計於2010年9月,也就是申報2010年的上半年度財報的時期,全面強制企業採取XBRL格式申報。具體措施條列如下:

乙、 建置加值資訊服務平台,提供更多資訊加值服務予使用者。

五、申報內容

一、 自願申報:四大財務報表(包含資產負債表、損益表、股東權益變動表及現金流量表)。

二、 全面申報:四大財務報表、會計師查核報告及財務報表附註。

六、申報方式與期限

自願申報與全面申報初期將採雙軌併行,未來再視實際運作情形,改採XBRL單軌申報。因此,本項計畫實施初期,允許XBRL格式資料之申報期限得以延後一個月,亦即在法規規定之期限內,以現有方式申報相關資料後,在原申報期限後一個月內再以XBRL格式申報相關資料。

以年度財務報告為例,法規規定之申報期限為每年的4月30日,故需於該期限內依現行方式公告並申報財務報告;XBRL格式之資料申報期限則為5月31日。

七、申報工具與軟體

配合主管機關推動XBRL申報財務報告,證交所規劃開發新一代XBRL財報編製軟體,免費提供上市櫃(興櫃)公司及會計師事務所使用。本軟體安裝於申報端個人電腦,提供友善而簡易的使用者操作介面,申報人員可選擇匯入XBRL、EXCEL及TXT等格式的檔案,或直接登打財務資料,完成資料檢核並產製 XBRL申報檔案後,透過公開資訊觀測站進行申報作業。

八、(附錄)國際資本市場應用現況

XBRL發展至今已近十年,且有越來越多的國家制定並發佈分類標準,實際應用於金融監理、稅務申報、電子化政府與工商管理方面,而證券市場之應用情形發展快速,以下簡單介紹各國應用的現況。

美國

係由證管會(SEC)主導XBRL計劃,美國證管會於2005年2月即開始執行自願性申報計畫(Voluntary Filing Program ),公司可於EDGAR以XBRL申報其財務資訊;2006年9月,美國證管會架設Interactive Financial Report Viewer網站,將XBRL格式之相關財務報告公布於網站上(http://216.241.101.197/viewer);2008年12月17 日,美國證管會通過一項新規範草案,將採循序漸進方式強制上市公司申報XBRL格式財務報告,其規範重點如下:

| 1 | 使用US GAAP的國內外大型加速申報公司(large accelerated filers,指由非關係人所持有的普通股總市值超過7億美元者),其普通股全球流通總市值(worldwide public equity float)超過50億美元者,必須以XBRL格式向SEC申報報表截止日在2009/6/15以後的財務報表、報表附註、說明性表格等,符合此標準的公司估計約有500家。 |

|---|---|

| 2 | 使用US GAAP的其他國內外大型加速申報公司(總市值超過7億美元、低於50億美元),延後一年實施與上述相同之規範。亦即必須將報表截止日在2010/6/15以後的財務報表、報表附註、說明性表格等內容以XBRL格式向SEC申報。 |

| 3 | 使用US GAAP的其他申報公司,以及使用IFRS的申報公司,再延後一年實施與上述相同之規範。亦即必須將報表截止日在2011/6/15以後的財務報表、報表附註、說明性表格等內容以XBRL格式向SEC申報。 |

| 4 | 除了申報XBRL格式財務報告外,公司仍須申報傳統格式(ascii、html)的財務報告。 |

| 5 | 第一次申報時,每項附註及每個說明性表格可分別可以一個文字區塊(a block of text)表達。但第二次申報開始,即須將內容細節以XBRL元素標籤標示出來。 |

加拿大

加拿大證券管理委員會(CSA)在2007年1月18日宣佈實施自願申報計畫,該計劃與美國證管會的Voluntary Filing Program相似。2007年5月SEDAR-加拿大公開發行公司之電子申報系統升級,現在已可接受XBRL格式之資料,2007年9月22日Newstrike Resources公司成為首家採用XBBL申報季報之公司。

南韓

韓國金融監督管理委員會在2006年8月展開自願申報計劃,共計有251家公司參與申報;2007年10月,韓國金融監督管理委員會的DART申報系統(以XBRL為基礎)開始上線,目前所有公開發行公司已強制採用XBRL申報其財務報告。

日本

日本是由金融廳主導XBRL計劃,由金融廳更新其EDINET申報系統,更新後該系統可接受XBRL格式的資料,2008年4月起所有公開發行公司申報全份財務報告時採用XBRL格式。另外,東京證券交易所配合金融廳的XBRL計劃,同步於2008年4月要求所有上市的公司須以XBRL申報決算短訊(Earning Digest)。

新加坡

新加坡是由會計與企業管理局(ACRA)主導XBRL計劃,並於2007年11月1日要求新加坡境內公司採用XBRL申報整份財務報告,目前所有公開發行及非公開發行公司已被要求以XBRL申報財務報告。

中國

是最早強制要求採用XBRL之國家,一開始是由上海證券交易所於2003年推動自願申報計劃,當時約有50家公司參與;此後,在2004年時申報第1季季報期間即已全面推廣採用XBRL申報財務報告摘要,而在2005年起也開始要求上市公司採用XBRL申報財務報告全文,目前已有超過800家上市公司採行。

西班牙

由該國證券主管機關-證券市場委員會(CNMV)自2005年開始實施上市公司自願申報計劃,2006年7月起IBEX 指數之35家公司即開始採用XBRL申報每季的財務報告,目前接受公開發行公司以XBRL申報其財務報表。

以色列

所有公開發行公司在編製2007年年度財務報告時,已採用IFRS(國際會計準則),以色列證券委員會同時也更新其電子申報系統(MAGNA),並將依據IFRS編製之會計資訊自動轉換為XBRL格式。

Taxonomy Development

Taiwan Stock Exchange started the taxonomy development for XBRL back in 2001 when the NII conducted a technical evaluation for such purpose. However, the effort was in vain, as there were no international standards established by then, and no authority in accounting could be served as a working partner. The Banking Bureau and Inspection Bureau adopted XBRL as the data interchange format in 2004 and 2005, respectively, to set up the platform and channel for financial supervision, and appointed the accounting industry in the country to establish the taxonomy data for financial supervision.

In 2005, Executive Yuan of the National Science Council launched the “Innovation in Cooperative Education Program” whereby inter-disciplinary research has been integrated on a much larger scale: “The e-integration of corporate financial information transparency and risk management in enterprises infrastructure” and the research program was established. Three seminars were held from January to March 2006. The seminars covered the contents of drafting the infrastructure of the XBRL industrial and commercial taxonomy modules, the taxonomy for account titles used in financial statements and notes to financial statements and the standard modules of materiality.

The complete XBRL standard framework for financial report in Taiwan was the result of tremendous efforts made in 2008 and 2009. The research team of the National Science Council consulted the “Statement of Financial Accounting Standards”, the “Standards for the Compilation of Financial Statements by Security Issuers”, the account titles used by general industry, the financial sector, the insurance industry, the securities industry, financial holding companies, and different operations in their consolidated financial statements and codes with relevant revision and matching tables, interviewed scholars and experts in the accounting and IT domain, and drafted the preliminary version of the standards for the classification of 4 major categories of financial statements for different industries.

The Taiwan Stock Exchange Corporation then held a number of public hearings to get the opinions of different sectors on the said standards. In addition, The Financial Supervisory Commission also invited the Accounting Research and Development Foundation, representatives of industrial and business organizations, the representatives of the CPA firms, scholars, experts, and the TWSE and Taipei Exchange to establish the “The Use of XBRL to Encourage Companies listed in TWSE, Taipei Exchange in Financial Reporting Task Force” comprising a number of work teams. These work teams are responsible for holding discussions on the standardization to ensure that the standards so adopted shall be applicable to the companies listed on TWSE, Taipei Exchange in the classification of financial reporting of different industries:

- 2008.12.25 Public Hearing for the Taxonomy development of the 4 financial statements in general industries

XBRL Standards for the classification of the 4 financial statements for general industries (December 25 2008 Public Hearing Version)

- 2009.1.9 Standardization Work Teams 1st meeting session for discussion on the standards for the classification of the 4 financial statements in general industries

- 2009.3.18 Standardization Work Teams 2nd meeting session for discussion on the standards for the classification of the 4 financial statements in general industries

- 2009.3.19 Public Hearing on the standards for the classification of the 4 financial statements for financial holding companies

XBRL Standards for the classification of the 4 financial statements for financial holding companies (March 19 2009 Public Hearing Version)

- 2009.3.25 Public Hearing on the standards for the classification of the 4 financial statements for financial industry

XBRL Stadnards for the classification of the 4 financial statements for the financial industry (March 25 2009 Public Hearing Version)

- 2009.3.30 Public Hearing on the standards for the classification of the 4 financial statements for the insurance industry

XBRL Standards for the classification of the 4 financial statements for the insurance industry (March 30 2009 Public Hearing Version)

- 2009.3.31 Public Hearing on the standards for the classification of the 4 financial statements for the securities industry

XBRL Standards for the classification of the 4 financial statements for the securities industry (March 31 2009 Public Hearing Version)

- 2009.4.2 Standardization Work Teams 3rd meeting session for discussion on the standards for the classification of the 4 financial statements in general industries

- 2009.6.5 Standardization Work Teams 4th meeting session for completion of revising the standards for the classification of the 4 financial statements in general industries

- 2009.7.7 Standardization Work Teams 5th meeting session for completion of revising the standards for the classification of the 4 financial statements in the financial industry

- 2009.7.8 Standardization Work Teams 6th meeting session for completion of revising the standards for the classification of the 4 financial statements in the insurance industry.

- 2009.7.9 Standardization Work Teams 7th meeting session for completion of revising the standards for the classification of the 4 financial statements in the securities and futures industry

- 2009.7.10 Standardization Work Teams 8th meeting session for completion of revising the standards for the classification of the 4 financial statements in financial holding companies.